Latent-Factor Models¶

This guide covers the structural latent-factor family:

PCAModelRPPCAModelIPCAModelCAEModel

These models all estimate latent structure, but they do not all use the same data contract or economic assumptions.

The family splits into two groups:

- persistent-panel estimators:

PCAModel,RPPCAModel - dated cross-sectional estimators:

IPCAModel,CAEModel

Overview¶

| Model | Contract | Loading structure | Predictive object |

|---|---|---|---|

PCAModel |

PersistentPanelBatch |

static loadings | beta × premium after a forecaster |

RPPCAModel |

PersistentPanelBatch |

static loadings with risk-premium-aware extraction | beta × premium after a forecaster |

IPCAModel |

CrossSectionBatch |

linear characteristic-implied betas | beta × premium after a forecaster |

CAEModel |

CrossSectionBatch |

nonlinear characteristic-implied betas | beta × premium after a forecaster |

PCA¶

PCAModel is the persistent-panel baseline.

Use it when:

- entity identity is stable through time

- variance decomposition is the primary structural task

- a simple low-dimensional baseline is more important than pricing-aware extraction

It estimates:

- static loadings

- factor returns from demeaned panel returns

It does not directly forecast expected returns. That requires:

- a factor-premium forecast

- an asset mapper

RP-PCA¶

RPPCAModel extends PCA by letting expected-return information influence factor extraction.

Conceptually, it moves from:

- explaining covariance only

to:

- explaining covariance and cross-sectional mean differences

This makes it attractive when you want factors that matter for pricing rather than only for variance decomposition.

The model follows Lettau and Pelger (2020): the extraction criterion blends covariance structure with pricing information instead of treating those as separate downstream concerns.

Key config fields:

gammabase_momentscale_by_asset_volatilitynormalize_loadingsorthogonalize_factors

IPCA¶

IPCAModel is the linear bridge between PCA and neural conditional factor models.

Economic idea:

- asset loadings are not static

- they are linear functions of observable characteristics

In the library, IPCAModel:

- consumes

CrossSectionBatch - alternates between factor estimation and gamma estimation

- returns a

LatentFactorStatewith conditional betas and factor history

The economic interpretation follows Kelly, Pruitt, and Su (2019): characteristics do not predict returns directly in an unconstrained way. They parameterize conditional factor exposures.

Predictive use:

- forecast factor premia from historical factor returns

- map current conditional betas times those premia back to assets

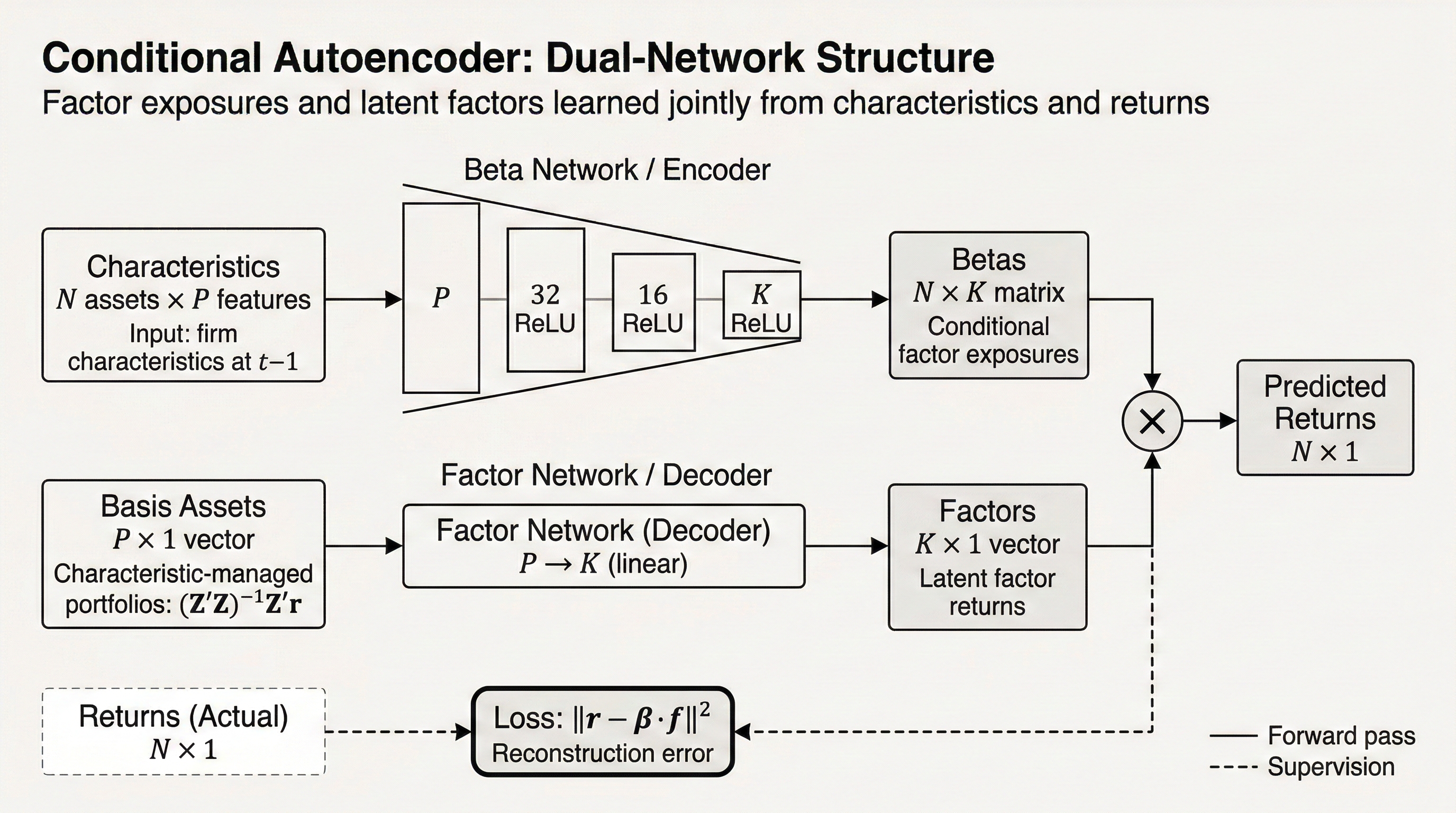

CAE¶

CAEModel is a conditional autoencoder structural extractor.

It should be interpreted as:

- a nonlinear extension of IPCA

- not as a direct supervised return predictor

The model learns:

- a nonlinear mapping from characteristics to betas

- latent factor returns from managed portfolios

The implementable return forecast is still a two-step object:

Current implementation features:

- configurable hidden units

- checkpoint-aware training

- optional ensemble averaging across saved checkpoints

- classification mode that still keeps factor construction tied to continuous returns

This is the right way to think about the model:

CAEModelis a nonlinear extension of IPCA- the fitted return uses realized latent factor returns

- the tradeable forecast replaces those realized factor returns with an ex ante premium estimate

That is exactly why CAEModel lives naturally inside

LatentFactorForecastPipeline rather than exposing a monolithic end-to-end return-prediction

API.

Persistent Vs Ragged¶

The split between panel and cross-sectional models is intentional.

Persistent-panel family¶

PCAModelRPPCAModel

Ragged cross-sectional family¶

IPCAModelCAEModel

This is not an implementation detail. It reflects the actual assumptions the models need.

If entity identity is unstable, use IPCAModel or CAEModel, not PCAModel or

RPPCAModel.

Recommended Defaults¶

Simple baseline¶

PCAModelorIPCAModelExpandingMeanFactorForecasterBetaLambdaMapper

Pricing-aware linear baseline¶

RPPCAModelExpandingMeanFactorForecasterBetaLambdaMapper

Nonlinear latent-factor baseline¶

CAEModelExpandingMeanFactorForecasterBetaLambdaMapper

Better-than-mean factor forecasting¶

Swap in:

AR1FactorForecasterEWMABaseFactorForecaster

without changing the structural model.