Latent-Factor Pipelines¶

The core latent-factor abstraction in ml4t-models is:

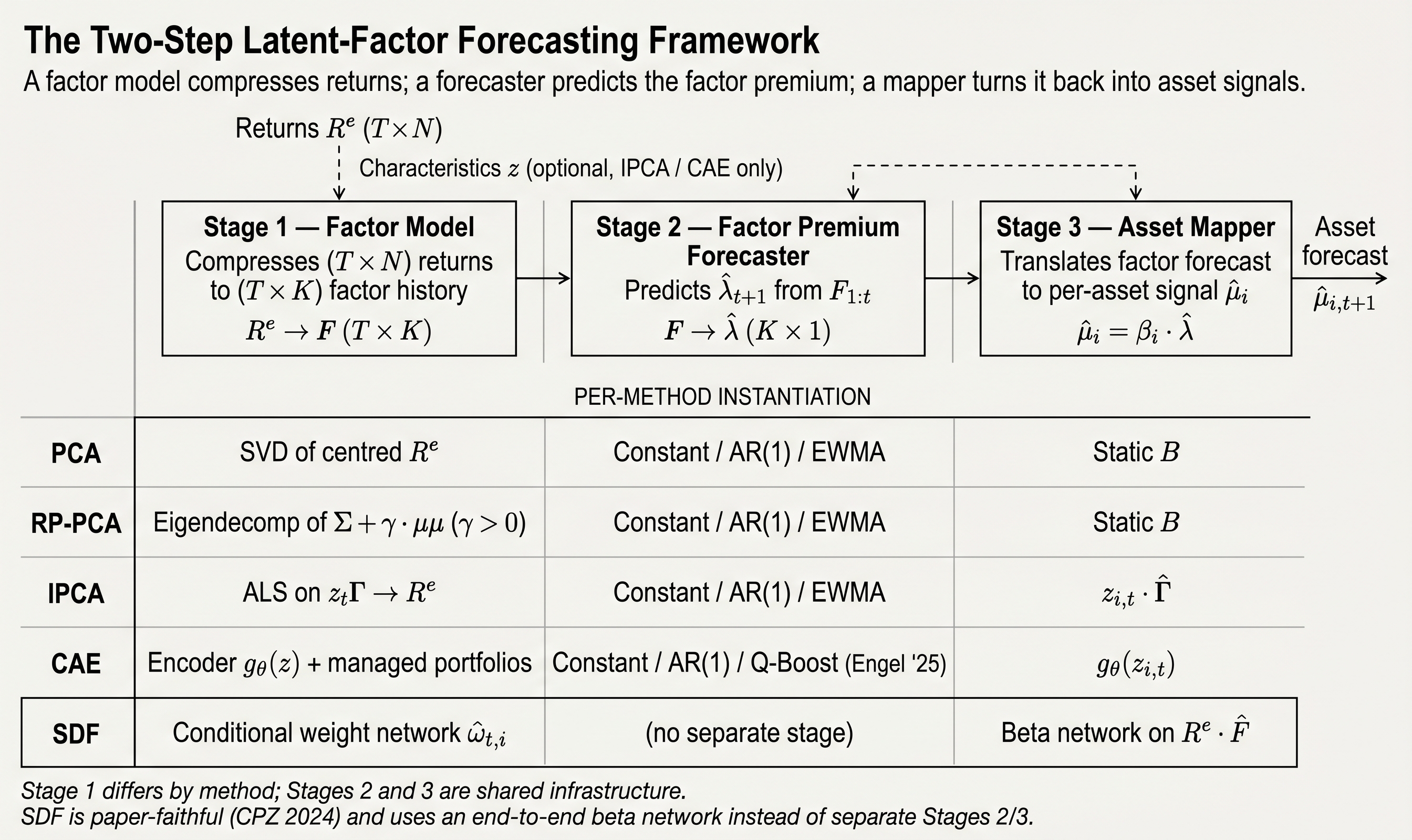

This keeps three distinct economic objects separate:

- exposures and factor realizations

- ex ante factor-premium forecasts

- asset-level expected returns

Why The Split Matters¶

For models like IPCA and CAE, the in-sample fitted return uses realized factor returns.

That is useful for reconstruction and attribution, but not directly for trading.

The implementable forecast replaces realized factor returns with a forecast or estimate of factor premia.

This distinction is the whole point of the two-step design:

- the structural model explains realized returns

- the forecaster produces an ex ante premium estimate

- the mapper turns today's exposures and that premium estimate into asset-level forecasts

That is the paper-faithful interpretation of IPCA and CAE.

Pipeline Class¶

LatentFactorForecastPipeline composes the three stages:

from ml4t.models import (

BetaLambdaMapper,

ExpandingMeanFactorForecaster,

IPCAConfig,

IPCAModel,

LatentFactorForecastPipeline,

)

pipeline = LatentFactorForecastPipeline(

model=IPCAModel(IPCAConfig(n_factors=3)),

forecaster=ExpandingMeanFactorForecaster(),

mapper=BetaLambdaMapper(),

)

Objects At Each Stage¶

Structural Model¶

Implements:

fit(batch) -> FitSummaryextract(batch, checkpoint=None) -> LatentFactorState

The extracted state contains:

asset_betas- optional

factor_returns - timestamps and asset IDs

- metadata such as the selected checkpoint

Factor Forecaster¶

Implements:

fit(state) -> FitSummarypredict(state) -> FactorForecastResult

Current forecasters:

ExpandingMeanFactorForecasterAR1FactorForecasterEWMABaseFactorForecaster

Asset Mapper¶

Implements:

predict(state, factor_forecast) -> AssetForecastResult

Current mapper:

BetaLambdaMapper

The Default Predictive Baseline¶

The simplest predictive latent-factor workflow is:

fit structural model on training data

estimate historical factor returns

forecast factor premia by the training-sample mean

map betas × premia back to assets

This is the baseline represented by:

ExpandingMeanFactorForecasterBetaLambdaMapper

The point of this baseline is clarity. It makes explicit what is structural estimation and what is factor-premium forecasting.

Beyond The Mean Baseline¶

The mean-premium forecast is a baseline, not a ceiling. The scalable-CAE literature argues that better forecasts of the latent factor series can improve the final asset-level signal.

The library therefore keeps the forecaster modular. You can swap in:

AR1FactorForecasterEWMABaseFactorForecaster

without changing the structural estimator.

The architectural point is more important than the specific forecaster list: structural estimation and factor-premium forecasting are separate layers.

Checkpoints¶

Neural structural models such as CAEModel expose configurable checkpoints:

checkpoint_intervalcheckpoint_epochsdefault_checkpoint

This lets you:

- extract structural states at multiple training horizons

- fit and evaluate downstream factor forecasters at those checkpoints

- choose reporting checkpoints explicitly rather than hard-coding hidden "best epoch" behavior

Diagram¶

flowchart LR

A[Batch] --> B[Structural Model]

B --> C[LatentFactorState]

C --> D[Factor Forecaster]

D --> E[FactorForecastResult]

C --> F[Asset Mapper]

E --> F

F --> G[AssetForecastResult]

G --> H[PredictionsFrame]

H --> I[ml4t-backtest / ml4t-diagnostic]When Not To Use This Pipeline¶

Do not force:

StochasticDiscountFactorModel- portfolio learners

- direct signal predictors

through this latent-factor composition. Those families solve different problems and have different native outputs.