Stochastic Discount Factor¶

StochasticDiscountFactorModel is a separate model family because the native object is not

a latent factor with a premium forecast. The native object is a weight-based pricing-kernel

proxy.

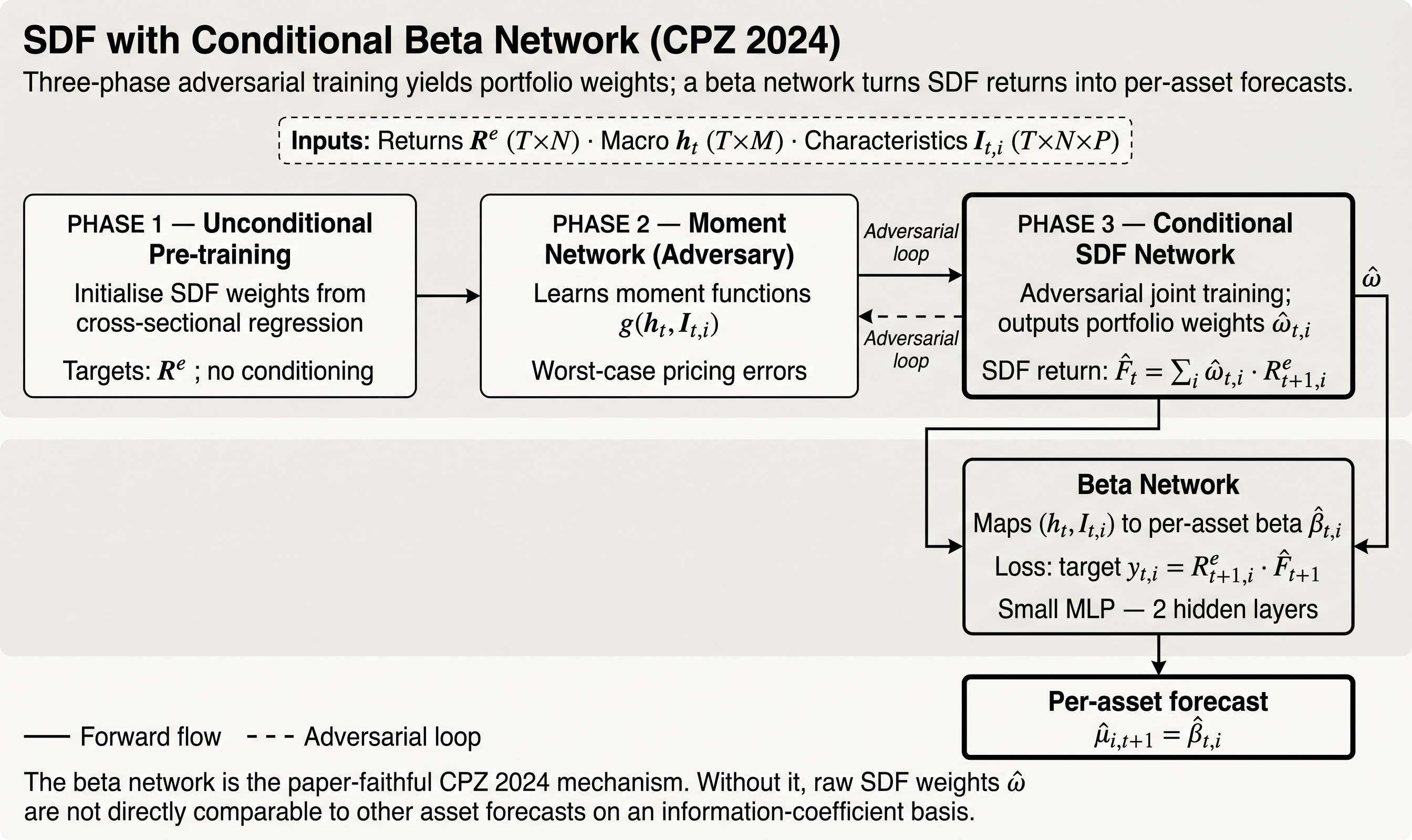

The implementation follows the phase-aware adversarial design of Chen, Pelger, and Zhu (2021): learn a pricing kernel that is disciplined by the most informative test-asset moments rather than only by reconstruction or covariance fit.

What The Model Estimates¶

The model is built around a no-arbitrage objective and returns:

asset_weights- optional realized

sdf_values - checkpoint-aware phase history

The public extracted state is:

StochasticDiscountFactorState

Why It Is Separate From Latent Factors¶

Latent-factor models estimate:

- exposures

- factor realizations

- then expected returns through

beta × premium

The stochastic discount factor family instead estimates a traded pricing object directly. It is closer to:

- a weight-learning model

- a no-arbitrage estimator

- a direct portfolio construction mechanism

That is why it lives under:

ml4t.models.stochastic_discount_factor

instead of under latent_factors.

Training Phases¶

The model is phase-aware:

- unconditional SDF training

- moment network fitting

- conditional SDF refinement

Key config fields:

n_epochs_uncn_epochs_momentn_epochs_condcheckpoint_epochsdefault_checkpoint

For the beta-head side:

beta_n_epochsbeta_checkpoint_epochsbeta_default_checkpoint

Native Output¶

The native output mode is:

weights

That is enforced by the current model implementation. If you want expected-return-style projections, use an explicit downstream mapper rather than treating expected returns as the primary estimation target.

Optional Return Mapping¶

Current helpers include:

LinearStochasticDiscountFactorReturnMapperStochasticDiscountFactorBetaNetworkHead

These are downstream transformations. They do not change the fact that the core estimator is weight-native.

The beta-network head is useful when you need an expected-return-like object for comparison with latent-factor studies, ranking experiments, or downstream backtests that expect asset predictions. It should still be documented as a secondary mapping, not as the primary SDF target.

Typical Workflow¶

from ml4t.models import CrossSectionBatch, StochasticDiscountFactorConfig, StochasticDiscountFactorModel

model = StochasticDiscountFactorModel(

StochasticDiscountFactorConfig(

checkpoint_epochs=(256, 512, 768, 1024, 1280),

default_checkpoint=1280,

)

)

fit_summary = model.fit(batch)

state = model.extract(batch)

Practical Interpretation¶

There are two common uses:

1. Trade The Weight Output Directly¶

Use the extracted asset weights as a cross-sectional allocation signal, subject to:

- leverage normalization

- caps

- liquidity filters

- turnover controls

2. Use A Beta-Or Return-Projection Head¶

If you need asset-level expected-return-like quantities for a downstream ranking or comparison study, use an explicit projection helper and document that it is a secondary object.

Checkpoints¶

Because the structural horizon is long, this family should usually use:

- explicit sparse

checkpoint_epochs

rather than dense interval checkpointing.

That keeps:

- extraction cost manageable

- beta-head retraining manageable

- model provenance easier to interpret

For that reason, the recommended default is sparse explicit checkpoint_epochs, not dense

interval checkpointing.